Key Takeaways

- FEHB coverage is generally available to eligible federal retirees who meet specific enrollment criteria.

- Understanding how FEHB coordinates with Medicare and the rules around changes is important for long-term health planning.

Many federal employees want to know how their health coverage changes when they retire. The Federal Employees Health Benefits (FEHB) program offers continuity, but eligibility and coverage details shift after you leave active service. Let’s walk through the essentials so you can feel more confident as you plan for retirement health benefits.

What Is FEHB for Retirees?

Overview of FEHB Program

The FEHB program is the primary health insurance system for most federal civilian employees and retirees. Managed by the U.S. Office of Personnel Management (OPM), FEHB gives you access to a range of health plans. You can choose from various coverage options for yourself and eligible family members, providing a base of medical protection that can carry into retirement if you meet the rules.

How FEHB Changes After Retirement

As a retiree, you can often keep FEHB coverage, but the way you participate changes. While you no longer pay premiums through payroll deduction, your access to the same plans and coverage remains—just through your retirement annuity. You must maintain continuous enrollment and satisfy certain service and enrollment requirements before stopping your federal job.

Core Principles Behind FEHB Coverage

At its core, FEHB for retirees is about providing ongoing group health protection at a group rate. The government continues to share in premium costs, as in your working years. This structure helps many retired federal workers avoid losing valuable coverage just because they shift from active employment to annuitant status, as long as they meet eligibility criteria.

Who Is Eligible for FEHB in Retirement?

Minimum Service and Enrollment Rules

To keep FEHB in retirement, you generally need to have:

- Retired with an immediate annuity (or under an early retirement authority)

- Been continuously enrolled (or covered as a family member) in any FEHB plan for at least five years before retiring, or for all federal service if less than five years

These are standard OPM requirements and are non-negotiable in most cases.

Key Exceptions to Eligibility

There are a few exceptions. For example, those retiring under specific disability provisions or as law enforcement officers may have slightly different qualifying paths. However, most retirees must meet the five-year coverage test. If you left government service but returned later and didn’t restore your FEHB, you may find yourself ineligible, highlighting the importance of continuous enrollment.

Can Survivors Maintain FEHB Coverage?

Yes, survivor annuitants—such as spouses or certain dependent children—can usually keep FEHB if the retiree elected survivor benefits and FEHB coverage before death. The survivor must continue to meet program requirements and pay any required premiums from the annuity.

How Does FEHB Coverage Work After Retirement?

What Stays the Same Post-Retirement?

Most aspects of your FEHB coverage remain unchanged as a retiree. You retain access to the same range of health plans as active employees, including self-only, self-plus one, and family options. The federal government generally continues to cover a portion of your monthly premium, providing stability as your workplace status shifts.

What Can Change With FEHB Benefits?

A few notable differences exist after retirement, including:

- Premiums are deducted from your retirement annuity rather than salary.

- You may no longer pay premiums on a pre-tax basis.

- Your coordination with other coverage, primarily Medicare, becomes relevant once you become eligible for Medicare.

Some life events (remarriage, death of a spouse, changes in dependent status) can also affect your eligibility or options.

Enrollment and Open Season Participation

Retirees can continue to participate in annual FEHB Open Season, allowing you to switch plans or change coverage levels. It’s important to pay attention to announcement periods—missing a window can restrict changes until the following year or a qualifying life event occurs.

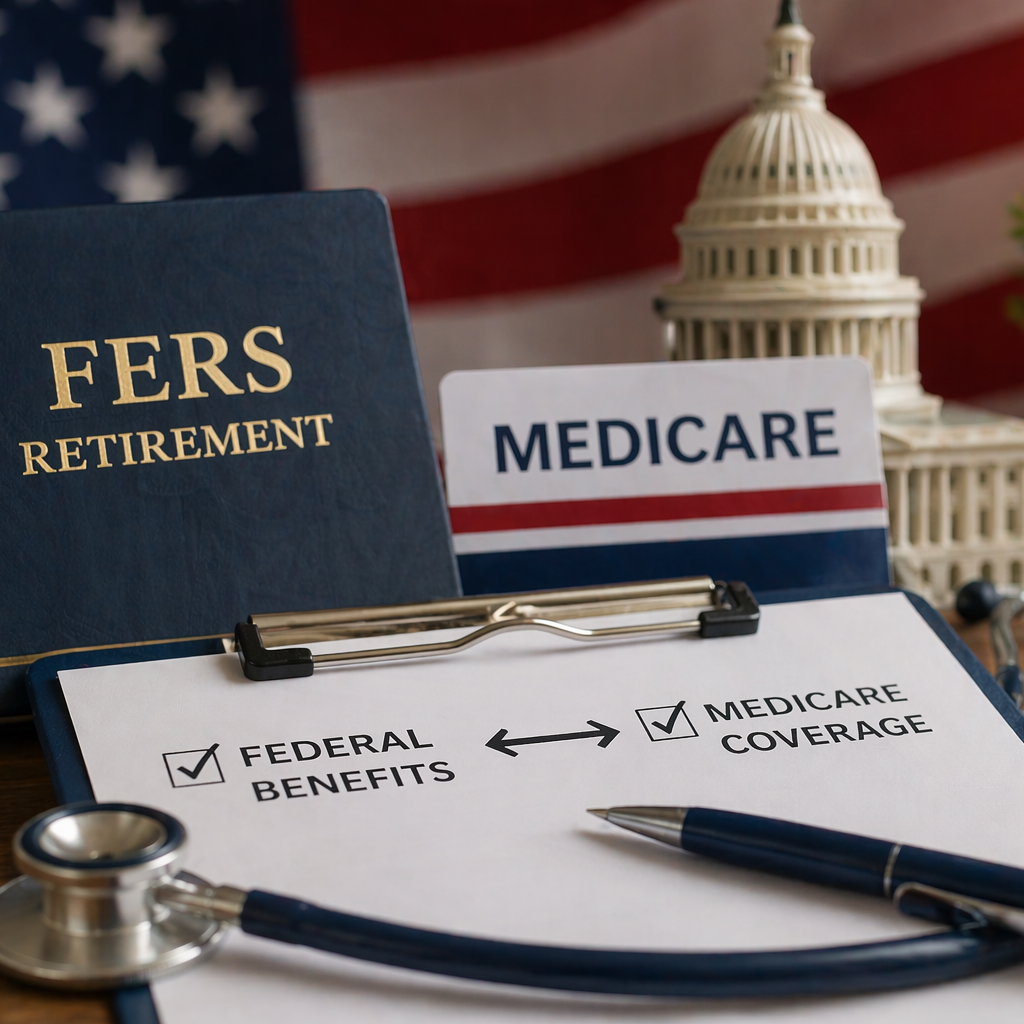

Do Retirees Need Medicare With FEHB?

Medicare Parts and Coordination

Many federal retirees become eligible for Medicare at age 65. Medicare has multiple parts—Part A (hospital insurance), Part B (medical insurance), Part D (prescription drug coverage), and more. FEHB can coordinate with these benefits, but you are not required to enroll in Medicare to keep your FEHB coverage.

How Medicare and FEHB May Interact

If you enroll in both FEHB and Medicare, coverage usually works together to reduce your out-of-pocket costs. Medicare typically acts as the primary payer, with FEHB as secondary. This setup can reduce co-pays and deductibles for covered services. Keep in mind that not all FEHB plans offer identical coordination with Medicare, so review plan brochures and OPM guidance for specifics.

Considerations for Different Health Needs

Deciding whether to enroll in Medicare Part B can depend on your health, existing coverage, and premium costs. Some retirees opt for full Medicare coordination, while others rely mostly on FEHB. Your circumstances and preferences play a role, but FEHB remains available whether or not you enroll in Medicare.

Are There Costs for Retiree FEHB Enrollment?

What Are the Typical Premium Arrangements?

FEHB premiums are based on the plan and covered tier (self, self plus one, family). After retirement, the federal government continues to pay a share of the premium, and you pay your portion, now through a deduction from your monthly annuity.

Paying FEHB Premiums After Retirement

Premiums for FEHB are typically withheld from your retirement annuity each month. If your annuity is not large enough to cover the full premium, OPM offers alternative payment arrangements, such as direct billing.

Potential Additional Costs to Consider

While your share of FEHB premiums persists, you may also experience increased costs if you lose access to pre-tax payment of premiums or add Medicare coordination. Out-of-pocket expenses, such as copays, deductibles, and plan-specific costs, also continue into retirement and may shift as your healthcare needs change.

Can You Make Changes to FEHB After Retirement?

Rules for Changing or Canceling FEHB

You have the right to change, reduce, or cancel FEHB coverage as a retiree, but significant restrictions apply. Unless you experience a qualifying life event, changes are generally only permitted during Open Season. Canceling FEHB can be permanent—once you leave, you may not be able to re-enroll.

Qualifying Life Events and FEHB Options

Common qualifying life events (QLEs) include marriage, divorce, birth of a child, or the loss of other health insurance. QLEs allow special mid-year changes to your FEHB coverage. Understanding which events apply to you helps you avoid losing coverage you need.

Common Enrollment Pitfalls to Avoid

One of the most frequent mistakes is canceling FEHB without understanding the permanent consequences. Another is missing Open Season deadlines for plan changes. Stay engaged with OPM announcements to avoid lapses in coverage.

What Should Federal Retirees Consider?

Weighing Health Needs and Coverage Options

Review your ongoing and anticipated health needs compared to your FEHB plan details. As your needs shift in retirement, you might benefit from a plan change during Open Season or coordination with Medicare.

Understanding Survivor Benefits

FEHB survivor coverage requires proper planning. If you want a spouse or child to continue coverage after your death, elect the correct annuity survivor options and keep FEHB active while living.

Long-Term Considerations With FEHB

Consider the effect of future premiums, plan changes, and possible legislative updates on your healthcare security. Although FEHB has been stable for decades, changes in family status or rules could impact your options down the line.

FEHB Retirement Eligibility: Common Questions

Is FEHB Guaranteed for All Retirees?

FEHB coverage in retirement is not automatically available to every federal retiree. You must satisfy OPM’s rules for continuous enrollment and retire under an immediate annuity. Otherwise, you may not qualify for post-retirement FEHB.

What If You Leave Federal Service Early?

Leaving federal service before being eligible for an immediate annuity or before completing the five-year enrollment period can disqualify you from FEHB coverage in retirement. It is important to review your employment history and enrollment timeline carefully.

Can Dependent Children Keep Coverage?

Dependent children can stay on your FEHB plan until they age out under program rules, typically at age 26. Certain conditions, like permanent disability, can allow continued coverage for adult children. OPM outlines these provisions in detail on its official site.