Key Takeaways

- Federal retirement planning errors often stem from misunderstood service records, pension calculations, and benefit elections.

- Becoming familiar with official guidance and carefully reviewing your records can help you avoid costly retirement mistakes.

Many federal employees have built careers of service, but even small mistakes in retirement planning can result in missed benefits or reduced income. Understanding where errors frequently happen can help you protect the financial security you’ve earned.

What Are Federal Retirement Planning Errors?

Common misconceptions about retirement benefits

Retirement under the federal system brings unique complexities. Some employees assume that simply reaching a certain age or completing a set number of years automatically qualifies them for full benefits. Others believe that all government service counts toward retirement in the same way, not realizing that part-time, temporary, or non-federal service may not meet credit requirements without extra steps.

Federal retirement forms and booklets often explain these details, but misconceptions persist. For example, many mistake the differences between the Civil Service Retirement System (CSRS) and the Federal Employees Retirement System (FERS), which can lead to incorrect benefit expectations.

Overview of federal retirement systems

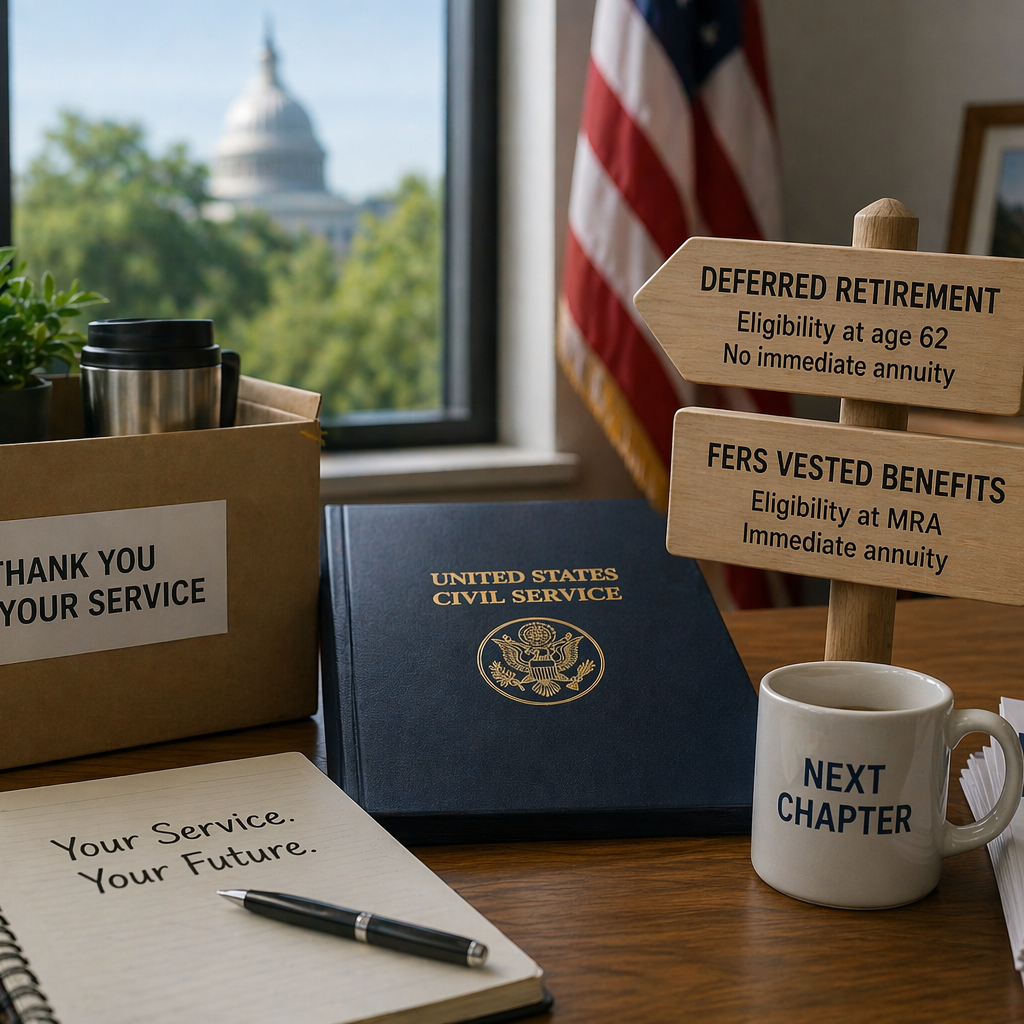

Most federal employees belong to one of two primary retirement systems: CSRS (for those hired before 1984) or FERS (for those hired in 1984 or later). Both systems provide a basic pension, but FERS also includes Social Security and the Thrift Savings Plan (TSP). Understanding which system you’re under is key to checking the details that affect your retirement.

Why Do These Mistakes Happen?

Complexity of federal retirement rules

Federal retirement programs rely on a web of rules spelled out in federal law and regulations. Each system—CSRS, FERS, TSP, FEHB—follows its own criteria for service credit, benefit calculations, and eligibility. The language in guidance documents can be technical, making it easy to overlook exceptions or misunderstand deadlines, especially for employees whose service spans several decades or agencies.

Misunderstood deadlines or requirements

Many errors arise when employees miss critical deadlines, such as the cut-off for making a service credit deposit or for electing survivor benefits. Sometimes, service history is incomplete, or a break in service gets overlooked. These issues are not always spotted until after retirement paperwork is submitted, which can make corrections harder to achieve.

Missing Service Credit: How Does It Affect You?

What is service credit?

Service credit refers to the total time in qualifying federal service that counts toward retirement eligibility and calculation. Not all periods of employment automatically accrue service credit. For example, temporary employment, certain types of military service, or part-time work may need to be verified or even purchased back to count fully.

Consequences of incomplete records

If your records do not reflect all allowable service, your pension calculation could be lower than you expect. Missing service credit can also delay when you become eligible for retirement or for continued health benefits. Sometimes, employees only realize there is missing service after they receive their annuity estimate or benefits statement—by then, some deadlines for correcting records may have passed.

Incorrectly Estimating Pension Amounts

FERS vs. CSRS calculation differences

CSRS and FERS use different formulas to calculate your monthly pension. CSRS generally provides a higher basic annuity, but FERS includes Social Security and TSP as additional sources. Estimating your benefit using the wrong system’s numbers can leave you with an inaccurate picture of your retirement income.

Factors that impact final benefit

Several items affect your pension:

- Length of creditable service

- High-3 average salary (the highest average basic pay over any three consecutive years)

- Retirement age

Mistakes can stem from assuming all earnings or time count equally, or overlooking reductions for early retirement, survivor elections, or unpaid service deposits.

Overlooking Survivor Benefit Elections

What are survivor options?

When you retire, you can elect to provide a monthly survivor benefit for a spouse or, in some cases, a former spouse. This election impacts your monthly annuity and must be made when you retire. Survivor options allow your selected beneficiary to receive a portion of your pension after your death.

Long-term impact of election choices

Failing to elect a survivor benefit at retirement usually means your spouse will not be eligible for ongoing payments, and returning later to change your election can be difficult or result in lower benefits. In some cases, court orders or federal requirements must be followed. Reviewing these options and understanding their impact before making final decisions is crucial.

Neglecting the Federal Thrift Savings Plan

Understanding TSP withdrawal rules

Your Thrift Savings Plan (TSP) is an important part of retirement under FERS, and TSP withdrawals come with rules for timing, types of payments, and required minimum distributions. Some retirees make uninformed choices about lump-sum withdrawals or regular payments, impacting how long their savings last.

Tax and timing considerations

TSP withdrawals are subject to federal tax, and there may be early withdrawal penalties if you access funds before certain ages. Timing your withdrawals to fit with monthly annuity payments, minimum distribution rules, and expected expenses in retirement can help maintain your financial stability—but only if you understand the rules in advance.

How Can You Avoid These Errors?

Double-checking official service records

Requesting your service history—often called a Certified Summary of Federal Service—before you retire can help ensure that gaps or errors are caught early. Verifying that all eligible periods of service are recorded and deposits are made for non-deduction service provides peace of mind and a more accurate basis for benefit calculations.

Reviewing OPM and agency guidance

Consulting official publications and agency-specific guidance helps clarify the retirement process. While rules may change, using up-to-date material from the Office of Personnel Management (OPM) and your HR office gives you the best chance of meeting deadlines and providing the documentation needed.

Are There Rules for Correcting Mistakes?

What OPM allows for corrections

The Office of Personnel Management has procedures in place for correcting errors in service records, benefit calculations, or election paperwork. Many issues, such as missing records or erroneous data, can be fixed if caught promptly. Employees and retirees generally need to provide official documentation, such as SF-50s, pay histories, or military records, to support corrections.

Deadlines for making changes

Certain corrections—such as service credit deposits or survivor elections—must be made before retirement, or within specified timeframes after separation. Missing these windows can limit your options and result in permanent reductions to benefits, so awareness of deadlines is essential.

Planning for Health Benefits in Retirement

Keeping FEHB into retirement

Maintaining your Federal Employees Health Benefits (FEHB) coverage into retirement is an option if you meet the eligibility requirements. Generally, you must have been enrolled in FEHB for at least five years immediately preceding your retirement. Failing to meet this condition could result in loss of health insurance as a retiree.

Medicare coordination considerations

Many federal retirees become eligible for Medicare. Deciding how to coordinate your FEHB coverage with Medicare Part A and Part B can affect your costs and coverage, but rules allow you to remain in FEHB while also enrolling in Medicare. Learning how these programs work together—by reviewing official resources—can help you make an informed choice and avoid discontinuity in your healthcare.