Key Takeaways

- Many federal retirement planning errors stem from misunderstandings of complex rules and recordkeeping.

- Regularly reviewing official records and understanding program options is key to avoiding costly mistakes.

Many federal employees pursue years of service with an eye on a secure retirement. However, mistakes—often avoidable—can disrupt even the most dedicated plans. By learning where others go wrong, you can take steps to stay on track and preserve your full benefits.

What Are Federal Retirement Planning Errors?

Common misconceptions about retirement benefits

Federal retirement benefits can be surprisingly nuanced. Some people believe they automatically qualify for all options after a set number of years. Others assume eligibility or benefits are the same across all agencies or career paths. These misconceptions often lead to overestimated benefits or missed opportunities: for instance, believing unused sick leave always counts toward service credit or assuming one is entitled to health benefits in retirement without meeting the required service threshold.

Overview of federal retirement systems

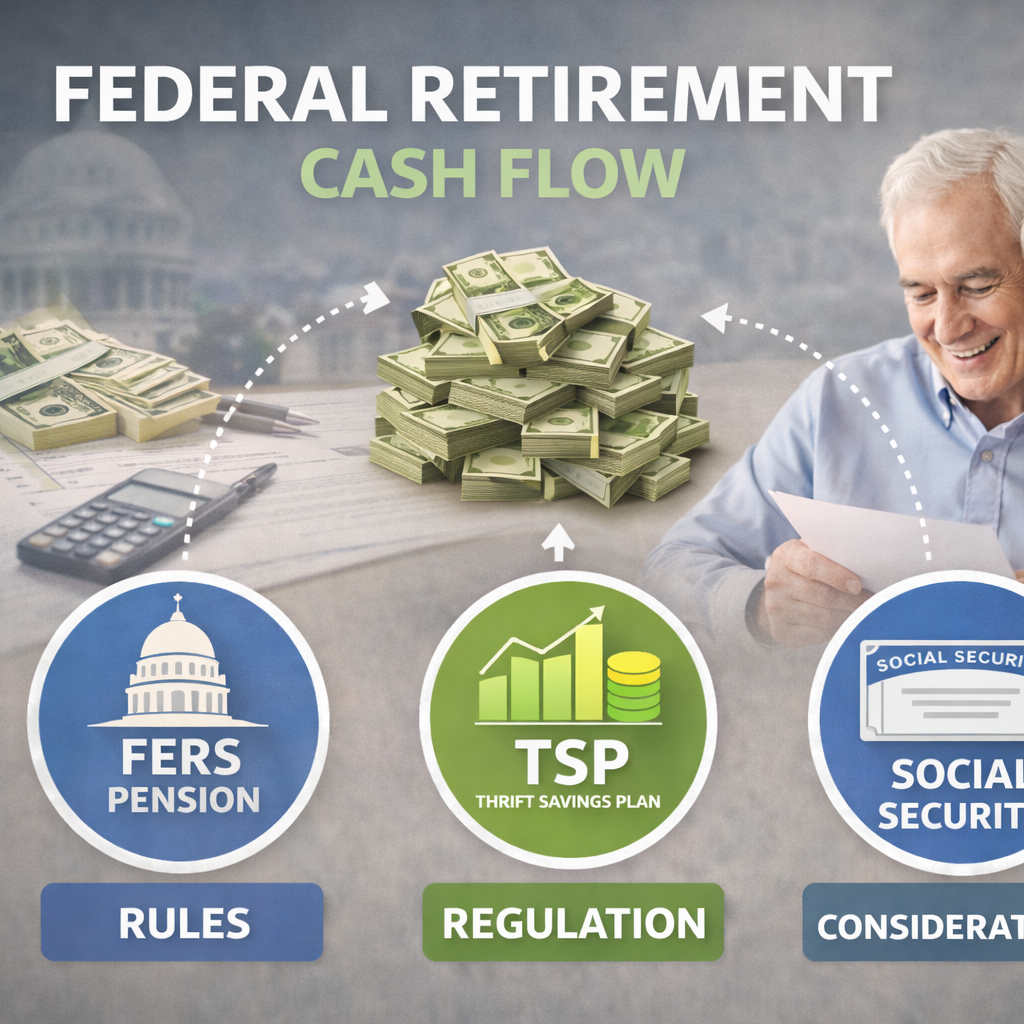

The federal workforce is covered primarily by two systems: the Civil Service Retirement System (CSRS) for those hired before 1984, and the Federal Employees Retirement System (FERS) for those hired after. Both offer pensions, but benefit calculations, eligible service, and other features differ. Most current employees and retirees are under FERS, which also includes Social Security and the Thrift Savings Plan (TSP) as key components. Knowing these systems’ rules is foundational for accurate retirement planning.

Why Do These Mistakes Happen?

Complexity of federal retirement rules

Federal retirement rules feature detailed eligibility requirements, complicated by exceptions for special categories (such as law enforcement or air traffic control). Changes in laws and regulations over the years, along with multiple benefit components, create confusion. It can be challenging to track how service breaks, different types of leave, or part-time schedules influence final calculations.

Misunderstood deadlines or requirements

Misunderstanding key requirements is common. For example, you need to carry Federal Employees Health Benefits (FEHB) coverage for at least five years before retirement to continue it afterward. Missing this window can result in losing access to FEHB. Deadlines for making survivor benefit elections or verifying service credit can also go overlooked amid busy pre-retirement periods.

Missing Service Credit: How Does It Affect You?

What is service credit?

Service credit refers to the officially documented periods that count toward your eligibility and calculation of your retirement benefit. Not all federal employment counts equally; certain temporary appointments, breaks in service, or unpaid leave may not automatically apply. Unused sick leave adds to total service under some but not all circumstances.

Consequences of incomplete records

Missing service credit reduces your total years used to calculate pension benefits. For instance, if you have several months uncredited due to a break in service or a temporary job, your pension amount—and sometimes even your eligibility date—can be directly impacted. Incomplete or inaccurate records can also delay processing of retirement claims, sometimes for many months.

Incorrectly Estimating Pension Amounts

FERS vs. CSRS calculation differences

CSRS and FERS use different formulas to determine your pension. CSRS typically provides a higher percentage of salary based on years of service and a specific accrual rate, while FERS uses a three-tiered approach: a smaller pension, Social Security, and TSP. Not recognizing which system you are under, or misunderstanding the formula, can lead to estimating a retirement benefit that does not match reality.

Factors that impact final benefit

Several factors shape your pension: length of creditable service, high-3 average salary (the highest average basic pay earned over any three consecutive years), retirement system, and survivor benefit deductions. Delays in updating your personnel file or failing to record promotions can cause undervaluation, while overestimating sick leave or miscounting part-time service may inflate your expectations.

Overlooking Survivor Benefit Elections

What are survivor options?

When you retire, you can choose whether to provide a survivor benefit for a spouse or eligible family member. This option, if elected, reduces your own monthly benefit but guarantees your survivor a portion (as defined by OPM regulations) after your passing. Declining this election can mean a one-time benefit payout or none at all, depending on your situation and choices made.

Long-term impact of election choices

Your survivor benefit election is binding at retirement unless certain life changes occur (such as marriage or divorce, subject to deadlines and documentation). An overlooked or misunderstood election may leave your spouse or dependent without vital income or the ability to maintain FEHB into widowhood. Reviewing your choices before finalizing them is essential.

Neglecting the Federal Thrift Savings Plan

Understanding TSP withdrawal rules

The Thrift Savings Plan (TSP) complements your pension and Social Security, giving you personal accountability for additional retirement savings. TSP withdrawal options and rules require careful review. For example, there are strict limitations on when and how you can take distributions, whether in the form of installments, partial withdrawals, or annuities. Failing to understand these can result in unnecessary taxes or reduced flexibility.

Tax and timing considerations

Withdrawals from TSP are generally subject to income tax, and the age at which you begin can affect both taxes owed and potential penalties. Failing to follow required minimum distribution rules may result in additional tax liabilities. Timing withdrawals without regard for these rules can result in an unexpectedly higher tax bill or restricted cash flow during retirement.

How Can You Avoid These Errors?

Double-checking official service records

Periodically reviewing your personnel records and service history helps catch omissions or inaccuracies early. Agencies maintain your Official Personnel Folder (OPF), which documents your appointments, leave, pay changes, and more. Verifying this data well before your planned retirement date reduces the chance of surprises or delays.

Reviewing OPM and agency guidance

OPM updates regulations, benefits eligibility criteria, and detailed guides regularly. Consulting these resources will clarify what counts toward service, when you can retire, and how benefits like survivor annuities or FEHB continuation apply. Your agency’s human resources portal often provides checklists and planning tools to help interpret these rules before any final decisions.

Are There Rules for Correcting Mistakes?

What OPM allows for corrections

OPM provides specific processes for correcting errors—such as recalculating service credit or amending a survivor benefit election—under certain conditions. For most changes, you must provide documented proof or complete designated forms. Some corrections (like adding prior service) take time, so acting promptly is important.

Deadlines for making changes

Many correction opportunities come with statutory deadlines. For example, survivor benefit elections generally must be made before or at retirement, with only a short window for post-retirement changes in specific scenarios. Missing a deadline could mean living with locked-in choices or reduced benefits, underscoring the need for timely review.

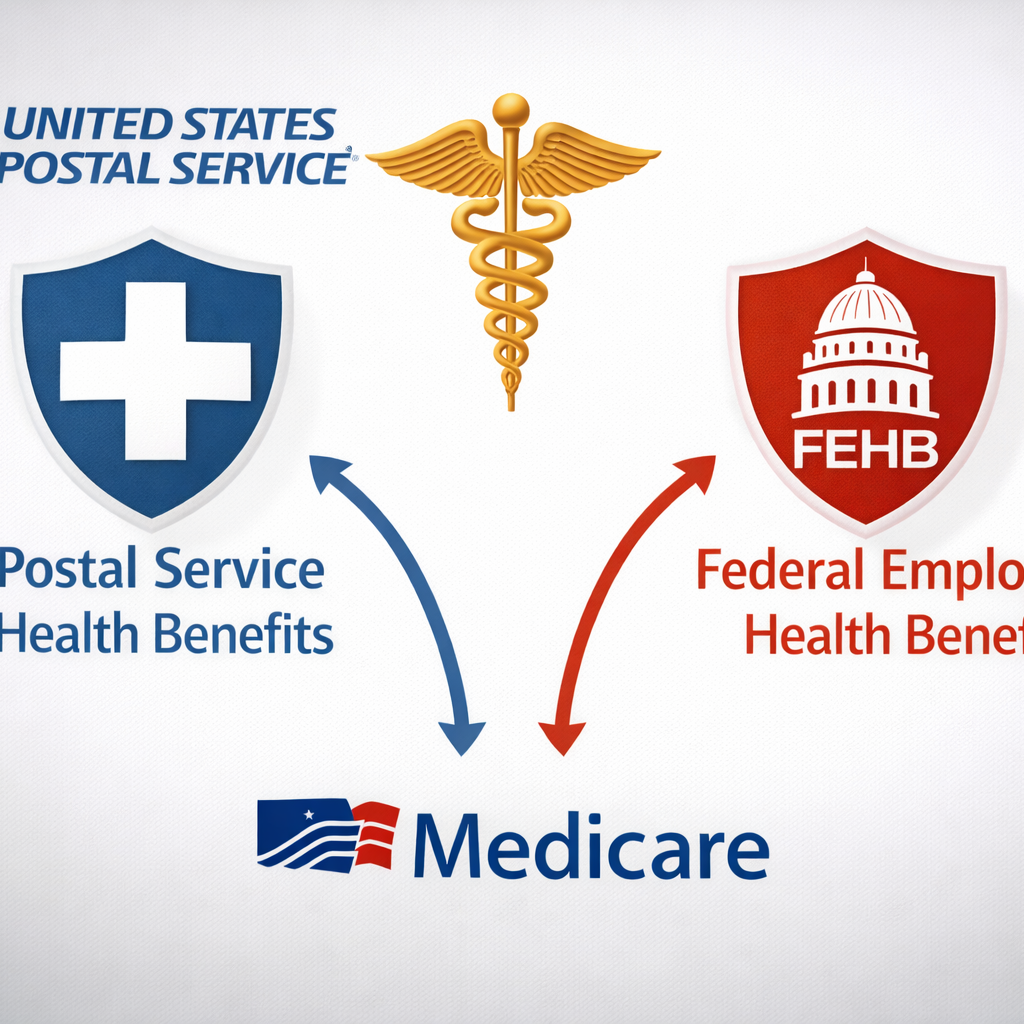

Planning for Health Benefits in Retirement

Keeping FEHB into retirement

Continuing FEHB requires five years of continuous enrollment before retirement. If you leave federal service before completing this period, you may forfeit eligibility to carry health coverage into retirement. This rule is strictly enforced by OPM.

Medicare coordination considerations

When you become eligible for Medicare, it’s important to understand how FEHB and Medicare work together. Many retirees choose to enroll in Medicare Part A while considering whether to add Part B. The decision can impact your total out-of-pocket costs and coverage—federal rules provide guidance on how these programs interact, especially in cases of dual coverage.